Q3 2024 Earnings Conference Call and Webcast Slides

PTC India

1. Event Update | Power

August 23, 2010

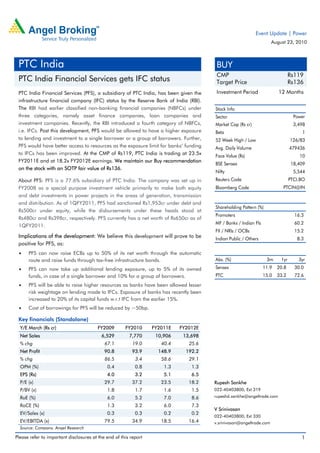

PTC India BUY

CMP Rs119

PTC India Financial Services gets IFC status Target Price Rs136

PTC India Financial Services (PFS), a subsidiary of PTC India, has been given the Investment Period 12 Months

infrastructure financial company (IFC) status by the Reserve Bank of India (RBI).

The RBI had earlier classified non-banking financial companies (NBFCs) under Stock Info

three categories, namely asset finance companies, loan companies and Sector Power

investment companies. Recently, the RBI introduced a fourth category of NBFCs, Market Cap (Rs cr) 3,498

i.e. IFCs. Post this development, PFS would be allowed to have a higher exposure Beta 1

to lending and investment to a single borrower or a group of borrowers. Further, 52 Week High / Low 126/83

PFS would have better access to resources as the exposure limit for banks’ funding Avg. Daily Volume 479436

to IFCs has been improved. At the CMP of Rs119, PTC India is trading at 23.5x Face Value (Rs) 10

FY2011E and at 18.2x FY2012E earnings. We maintain our Buy recommendation

BSE Sensex 18,409

on the stock with an SOTP fair value of Rs136.

Nifty 5,544

About PFS: PFS is a 77.6% subsidiary of PTC India. The company was set up in Reuters Code PTCI.BO

FY2008 as a special purpose investment vehicle primarily to make both equity Bloomberg Code PTCIN@IN

and debt investments in power projects in the areas of generation, transmission

and distribution. As of 1QFY2011, PFS had sanctioned Rs1,953cr under debt and

Shareholding Pattern (%)

Rs500cr under equity, while the disbursements under these heads stood at

Promoters 16.3

Rs480cr and Rs398cr, respectively. PFS currently has a net worth of Rs650cr as of

MF / Banks / Indian Fls 60.2

1QFY2011.

FII / NRIs / OCBs 15.2

Implications of the development: We believe this development will prove to be Indian Public / Others 8.3

positive for PFS, as:

• PFS can now raise ECBs up to 50% of its net worth through the automatic

route and raise funds through tax-free infrastructure bonds. Abs. (%) 3m 1yr 3yr

• PFS can now take up additional lending exposure, up to 5% of its owned Sensex 11.9 20.8 30.0

funds, in case of a single borrower and 10% for a group of borrowers. PTC 15.0 33.2 72.6

• PFS will be able to raise higher resources as banks have been allowed lesser

risk weightage on lending made to IFCs. Exposure of banks has recently been

increased to 20% of its capital funds w.r.t IFC from the earlier 15%.

• Cost of borrowings for PFS will be reduced by ~50bp.

Key financials (Standalone)

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Net Sales 6,529 7,770 10,906 13,698

% chg 67.1 19.0 40.4 25.6

Net Profit 90.8 93.9 148.9 192.2

% chg 86.5 3.4 58.6 29.1

OPM (%) 0.4 0.8 1.3 1.3

EPS (Rs) 4.0 3.2 5.1 6.5

P/E (x) 29.7 37.2 23.5 18.2 Rupesh Sankhe

P/BV (x) 1.8 1.7 1.6 1.5 022-40403800; Ext 319

RoE (%) 6.0 5.2 7.0 8.6 rupeshd.sankhe@angeltrade.com

RoCE (%) 1.3 3.2 6.0 7.3

V Srinivasan

EV/Sales (x) 0.3 0.3 0.2 0.2

022-40403800; Ext 330

EV/EBITDA (x) 79.5 34.9 18.5 16.4 v.srinivasan@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. PTC India | Event Update

PFS’s shareholding pattern

PTC India holds a 77.6% stake in PFS, whereas the remaining 22.4% is shared

equally by Goldman Sachs Strategic Investments Limited (GSSI) and Macquarie

Group Limited (Macquarie).

Exhibit 1: PFS’s shareholding pattern (%)

11.2

11.2

77.6

PTC GSSI Macquarie

Source: Company, Angel Research

Exhibit 2: Project portfolio (Equity stake)

Project Location Details Stake (%)

Renewable energy

10MW biomass Maharashtra Project commissioned in FY2009 26

plant

100MW wind cum Maharashtra 41.25MW first phase to be commissioned in August 2010; 58.75MW second 37

bio-diesel project phase to be commissioned in December 2010

SPV to undertake - This SPV will scout for investment opportunities across the country. Around 50 Up to 26

500MW biomass projects have already been identified, out of which permissions for 25

and renewable projects have been received from the state government. One project is in the

energy projects process of acquisition.

3MW solar Haryana The entire land for the project has been identified and the MoU has been 37

power project signed with HAREDA. Order for equipment has been placed, which is likely to

be commissioned by December 2010.

Conventional energy

189MW imported Tamil Nadu The project is a merchant power plant and has three units of 63MW each. 26

coal project The first two units have been commissioned. The last unit is in the

synchronization stage.

270MW imported Andhra Pradesh This is a tolling project in which PTC India will be supplying coal to the 26

coal project project and will purchase power by paying conversion charges. Financial

closure for the projects has been achieved. The project is expected to be

commissioned by CY2011.

Stage 1 of Andhra Pradesh 70% of coal required for the project has got the linkage from Ministry of NA

2x660MW Coal, GOI. The required land for the project has already been acquired. The

thermal project project is expected to be commissioned by 2012.

2x350MW Orissa It is a domestic pit-head coal project, for which coal linkage has already NA

thermal project been obtained. Financial closure for the first unit has been achieved and that

for the second unit is in advanced stages. The first unit and second units are

expected to be commissioned by December 2011 and March 2012,

respectively.

Source: Company, Angel Research

August 23, 2010 2

3. PTC India | Event Update

PFS financial performance in FY2010

PFS recorded net sales of Rs49cr in FY2010, up 372% on a yoy basis. The

company’s EBITDA and PBDT rose by 487% and 323% to Rs43.6cr and Rs36.7cr,

respectively. Growth was largely driven by higher level of loan disbursement (both

term loan and mezzanine/short-term loan) to power projects and increased

fee-based income. During FY2010, the company sanctioned funds aggregating to

~Rs1,510cr to 22 power projects. During the year, the company also started

upfront financing for carbon credits.

Exhibit 3: PFS’s financial performance

(Rs cr) FY2010 FY2009 Chg [%]

Gross Sales 48.8 10.3 372

Net Sales 48.8 10.3 372

Other Income 4.7 1.3 270

Total Income 53.5 11.6 361

Total Expenditure 5.2 2.9 79

EBITDA 43.6 7.4 487

Interest 11.6 0.0 -

PBDT 36.7 8.7 323

Depreciation 0.0 0.0 -

Tax 11.3 0.2 -

Reported PAT 25.5 8.5 198

Equity Capital 435 435 -

Reserves and Surplus 200 175 14.3

Source: Company, Angel Research

August 23, 2010 3

4. PTC India | Event Update

Investment arguments

Power deficit to encourage growth

The total volume of power traded in India is just 8% of the power generated, as

reported by the power ministry in 2010. We expect the volume of power traded to

rise at a healthy rate of 14% due to the continuing power deficit and increased

power generation capacity.

Favourable government policies to aid growth

The National Electricity Policy encourages about 15% of new capacities to be tied

up in the short-term market. Growing emphasis on allowing open access to

consumers to buy power from producers in any state augurs well for power trading

companies, such as PTC India.

In January 2010, the CERC had increased the cap on short-term trading margin to

7paise/unit from the earlier 4paise/unit, which is a major boost to profitability as

the 4paise/unit cap regime was inadequate to cover the operational and market

risks borne by trading companies.

PTC India to maintain its market leadership position

PTC India is currently the leader in power trading with a market share of 45–50%.

Going ahead, we expect the company to maintain its leadership position in the

power trading market on account of its early-mover advantage and increased

volume of power traded under the long-term trade route, as close to 4,500MW of

projects for which the company has signed PPAs are set to be operational in

FY2011 and FY2012.

Transforming into an integrated player in the power sector

Apart from power trading, PTC India has also entered into other businesses such

as financing fuel intermediation, power tolling agreements and consultancy. PFS

has expanded its business considerably in the past two years.

PTC India, through its subsidiaries, is also looking at acquiring coal mines abroad

to aid its fuel intermediation and power tolling business.

August 23, 2010 4

5. PTC India | Event Update

Outlook and valuation

Going ahead, we believe PTC India's emphasis on the long-term trade (LTT)

segment will help it in sustaining higher growth. During FY2010, STT constituted

50% of the total power traded by the company. PTC India proposes to increase its

power trading mix to 70:30 in favour of LTT. The company's increased focus on

LTT is expected to provide consistent cash flows compared to STT, as the number

of units generated is expected to be uniform, resulting in reduced volatility.

Following the commissioning of new power projects, we expect PTC India to

register a 32.7% CAGR in its top line over FY2010–12E. We estimate the

company’s bottom line to register a 43.1% CAGR over FY2010–12E.

At the CMP of Rs119, PTC India is trading at 23.5x FY2011E and 18.2x FY2012E

earnings. We have arrived at an SOTP fair value of Rs136 for PTC India, wherein

we have assigned P/E of 10x FY2012E earnings from the core trading business

(Rs65.2/share), while investments in PFS, Teesta Urja, Krishna Godawari and

Athena Energy Ventures have been valued at P/BV of 1x FY2012E (Rs49.4/share).

The cash and liquid investments in the company's books are valued at P/BV of 1x

FY2012E (Rs21.1/share). Accordingly, we maintain our Buy recommendation on

the stock.

Exhibit 4: SOTP-based target price

Particulars Valuation parameter Per share value (Rs)

Core Business – Power Trading 10x FY2012E earnings 65.2

Cash and Liquid Investments 1x FY2012E book value 21.1

Investments in Subsidiaries, Associates 1x FY2012E book value 49.4

Target Price 135.7

Source: Angel Research

August 23, 2010 5

6. PTC India | Event Update

Profit and loss statement (Standalone)

Y/E March (Rs cr) FY2007 FY2008 FY2009 FY2010 FY2011E FY2012E

Net Sales 3,767 3,906 6,529 7,770 10,906 13,698

Other operating income - - - - - -

Total operating income 3,767 3,906 6,529 7,770 10,906 13,698

% chg 21.2 3.7 67.1 19.0 40.4 25.6

Total Expenditure 3,736 3,887 6,503 7,707 10,770 13,524

Net Raw Materials 3,661 3,808 6,386 7,675 10,554 13,253

Other Mfg costs 4 3 - 0 5 7

Personnel 5 7 15 18 17 22

Other 67 69 101 13 193 242

EBITDA 30 19 26 64 136 174

% chg (35.6) (36.9) 36.6 143.7 114.5 27.6

(% of Net Sales) 0.8 0.5 0.4 0.8 1.3 1.3

Depreciation& Amortisation 1 1 6 6 8 8

EBIT 29 18 20 58 129 166

% chg (36.5) (38.5) 10.8 193.8 121.4 29.3

(% of Net Sales) 0.8 0.5 0.3 0.7 1.2 1.2

Interest & other Charges 3 2 4 0 5 6

Other Income 19 43 97 74 83 102

(% of PBT) 0.5 0.8 0.9 0.6 0.4 0.4

Share in profit of Associates - - - - - -

Recurring PBT 39 52 113 131 207 262

% chg (24.6) 31.7 119.8 15.8 57.4 26.6

Extraordinary Expense/(Inc.) (7) (7) - (0) - -

PBT (reported) 46 59 113 132 207 262

Tax 11 10 23 38 58 69

(% of PBT) 27.1 19.8 19.9 28.7 28.0 26.5

PAT (reported) 35 49 91 94 149 192

PAT after MI (reported) - - - - - -

ADJ. PAT 29 41 91 94 149 192

% chg (19.8) 44.9 119.5 3.0 59.1 29.1

(% of Net Sales) 0.8 1.1 1.4 1.2 1.4 1.4

Basic EPS (Rs) 2 2 4 3 5 7

Fully Diluted EPS (Rs) 2 2 4 3 5 7

% chg (11.4) (8.5) 86.5 (20.1) 58.6 29.1

August 23, 2010 6

10. PTC India | Event Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement PTC India

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock No

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

August 23, 2010 10

11. PTC India | Event Update

Address: Acme Plaza, ‘A’ Wing, 3rd Floor, M.V. Road, Opp. Sangam Cinema, Andheri (E), Mumbai - 400 059.

Tel: (022) 3952 4568 / 4040 3800

Research Team

Fundamental:

Sarabjit Kour Nangra VP-Research, Pharmaceutical sarabjit@angeltrade.com

Vaibhav Agrawal VP-Research, Banking vaibhav.agrawal@angeltrade.com

Vaishali Jajoo Automobile vaishali.jajoo@angeltrade.com

Shailesh Kanani Infrastructure, Real Estate shailesh.kanani@angeltrade.com

Anand Shah FMCG, Media anand.shah@angeltrade.com

Deepak Pareek Oil & Gas deepak.pareek@angeltrade.com

Sushant Dalmia Pharmaceutical sushant.dalmia@angeltrade.com

Rupesh Sankhe Cement, Power rupeshd.sankhe@angeltrade.com

Param Desai Real Estate, Logistics, Shipping paramv.desai@angeltrade.com

Sageraj Bariya Fertiliser, Mid-cap sageraj.bariya@angeltrade.com

Viraj Nadkarni Retail, Hotels, Mid-cap virajm.nadkarni@angeltrade.com

Paresh Jain Metals & Mining pareshn.jain@angeltrade.com

Amit Rane Banking amitn.rane@angeltrade.com

John Perinchery Capital Goods john.perinchery@angeltrade.com

Jai Sharda Mid-cap jai.sharda@angeltrade.com

Sharan Lillaney Mid-cap sharanb.lillaney@angeltrade.com

Amit Vora Research Associate (Oil & Gas) amit.vora@angeltrade.com

V Srinivasan Research Associate (Cement, Power) v.srinivasan@angeltrade.com

Aniruddha Mate Research Associate (Infra, Real Estate) aniruddha.mate@angeltrade.com

Mihir Salot Research Associate (Logistics, Shipping) mihirr.salot@angeltrade.com

Chitrangda Kapur Research Associate (FMCG, Media) chitrangdar.kapur@angeltrade.com

Vibha Salvi Research Associate (IT, Telecom) vibhas.salvi@angeltrade.com

Pooja Jain Research Associate (Metals & Mining) pooja.j@angeltrade.com

Yaresh Kothari Research Associate (Automobile) yareshb.kothari@angeltrade.com

Shrinivas Bhutda Research Associate (Banking) shrinivas.bhutda@angeltrade.com

Sreekanth P.V.S Research Associate (FMCG, Media) sreekanth.s@angeltrade.com

Hemang Thaker Research Associate (Capital Goods) hemang.thaker@angeltrade.com

Technicals:

Shardul Kulkarni Sr. Technical Analyst shardul.kulkarni@angeltrade.com

Mileen Vasudeo Technical Analyst vasudeo.kamalakant@angeltrade.com

Derivatives:

Siddarth Bhamre Head - Derivatives siddarth.bhamre@angeltrade.com

Jaya Agarwal Derivative Analyst jaya.agarwal@angeltrade.com

Institutional Sales Team:

Mayuresh Joshi VP - Institutional Sales mayuresh.joshi@angeltrade.com

Abhimanyu Sofat AVP - Institutional Sales abhimanyu.sofat@angeltrade.com

Nitesh Jalan Sr. Manager niteshk.jalan@angeltrade.com

Pranav Modi Sr. Manager pranavs.modi@angeltrade.com

Sandeep Jangir Sr. Manager sandeepp.jangir@angeltrade.com

Ganesh Iyer Sr. Manager ganeshb.Iyer@angeltrade.com

Jay Harsora Sr. Dealer jayr.harsora@angeltrade.com

Meenakshi Chavan Dealer meenakshis.chavan@angeltrade.com

Gaurang Tisani Dealer gaurangp.tisani@angeltrade.com

Production Team:

Bharathi Shetty Research Editor bharathi.shetty@angeltrade.com

Simran Kaur Research Editor simran.kaur@angeltrade.com

Bharat Patil Production bharat.patil@angeltrade.com

Dilip Patel Production dilipm.patel@angeltrade.com

August 23, 2010 11